Masters of the Universe category archive

Broke Banks 0

Atrios explains how banking works.

The Fee Hand of the Market 0

The game of Fee Card Monte continues:

The Pew study found that more than half of those hit with overdraft fees did not believe they had opted in to the policies, which enable banks to approve purchases or withdrawals for customers short of funds and then charge them fees for the transactions. Pew says the median bank overdraft fee is about $35.

One is tempted to say, “Read those statements banks send you about ‘changes to the agreement’ carefully,” but, really, that’s pointless advice.

If you have a magnifying glass strong enough to make that four-point type legible, you find quickly that the prose is a multi-syllabic word salad that even Sarah Palin would step back to admire. Follow the link for a description of some of the semantic games banks play.

Here’s the two magic words for avoiding this.

Pay cash.

I don’t mean pay cash for everything; that’s an absurdist fantasy attractive only to those who fancy themselves “Libertarians.”*

I mean pay cash for that cup of coffee. Pay cash for those three bags of chips from the dollar store. Pay cash for anything under twenty dollars.

Aside: I used to wonder how persons kept track of all those itsy-bitsy debit card purchases. Then I read about the banks’ Fee Card Monte and realized: they can’t; that’s what the banks are banking on, to the tune of $30,000,000,000 in overdraft fees last year.

Will paying cash automatically keep your pocket from being picked?

No. It will make keeping track of your checkbook a lot easier. Then you can keep yourself from overdrawing your account.

_________________________

*Libertarian: A Republican who’s ashamed to admit it.

Update from the Foreclosure-Based Economy 0

Bloomberg:

Now it turns out some lenders haven’t merely been unhelpful; their actions have pushed some borrowers over the foreclosure cliff. Lenders have been imposing exorbitant insurance policies on homeowners whose regular coverage lapses or is deemed insufficient. The policies, standard homeowner’s insurance or extra coverage for wind damage, say, for Florida residents, typically cost five to 10 times what owners were previously paying, tipping many into foreclosure.

When I bought my truck, my lender tried to pull a stunt like this with my car insurance. Only I had insurance already–I had to show proof of insurance to drive the thing off the lot.

Their policy’s premiumn was four times mine.

It took me three months to get them to stop trying to swindle me. The car salesman, who was a neighbor of mine, later told me that he had heard that this was not an uncommon problem with them.

And they were not some finance company.

They were an old local bank.

UnAmerican Activities Deportment 0

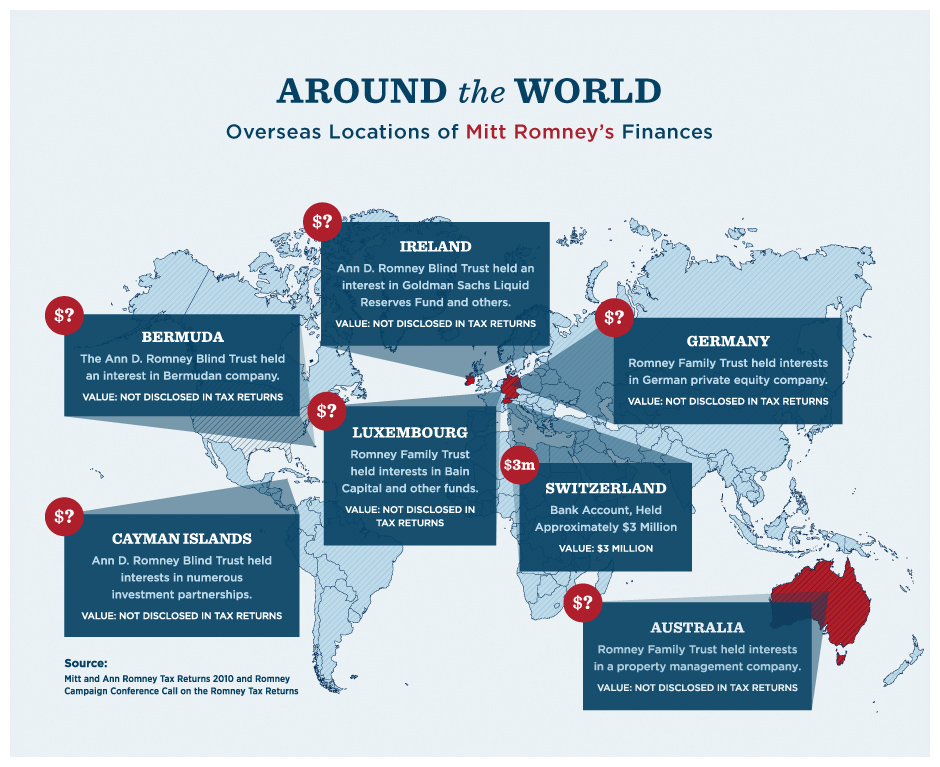

At MarketWatch, Al Lewis (no, not that Al Lewis) takes a scathing look at those who give up their US citizenship so they don’t have to pay taxes. A nugget:

Caught between your money and your country, you chose your money. You sold your American soul.

Read the rest.

Dustbiters 0

The FDIC is still managing to find some nuggets to munch on.

Hidden in Plain Sites 0

Update from the Foreclosure-Based Economy 0

Banks aren’t sure this is a good idea.

The director of the Consumer Financial Protection Bureau is aiming to discourage lenders from making home loans with risky features and outlining steps they must take to verify borrowers’ finances, as part of the “qualified mortgage” or QM regulation. Banks that follow the guidelines will gain legal protection against borrower defaults.

“Here’s what should be the least surprising lending advice you’ve ever heard: If you are going to lend money, you should probably care about getting paid back,” Raj Date, the agency’s deputy director, said in a speech April 20 in Los Angeles.

Could it be that they fear it might impede the pace of foreclosures mortgage sales commissions? Read the rest to find out.

The New Debtors’ Prisons 0

Steven D. reports on the 21st century version.

Update from the Foreclosure-Based Economy 0

Why the effrontery of these people! How dare they take the initiative!

The banks, natch, are against this. They want to be able to foreclose just on their say-so.

We know how well that has worked out.

Pay for Performance 0

As designed by Dillinger and Assocs, Compensation Consultants:

Likewise, CEO pay at the companies on the Fortune 500 list rose four times faster than the firms’ combined profits, which squeaked up barely 7 percent in five years.

Dustbiters 0

More masters of the universe are out of their jobs–so routine I don’t even check for the list on Friday evening any more:

-

HarVest Bank of Maryland, Gaithersburg, Maryland

Inter Savings Bank, fsb D/B/A Interbank, fsb, Maple Grove, Minnesota

The first two on the list deserved punishment for crimes against spelling, regardless of their fiduciary behaviour.

In related news, some of our local masters of the universe are facing time. I suspect that they are not so special as to be the only ones deserving of that privilege.

Dustbiter 0

The FDIC is still finding the occasional bank to blank.

Meanwhile, in my local rag, more news of responsible fiscals:

A Modest Proposal 0

This should work out nicely.

From Bloomberg:

A segment of the population with a well-established reputation for trustworthi–oh, never mind.

Another One Bites the Dust 0

Yesterday’s bank failure:

The trickle of failure is the actual trickle of trickle-down trickery.

Too Big To Jail? 0

Aside:

Being rich seems to be its own “Get Out of Jail Free” card.

Of course, it makes sense if you believe that wealth is a sure sign of virture.

Update from the Foreclosure-Based Economy 0

Soon to be replaced by the eviction-based economy:

But as a deal, this one is tilted to the banks.

That’s certainly the takeaway from the bank’s announcement Friday that it would offer borrowers a chance to turn over their homes to B. of A. in exchange for a deal where the bank would rent those properties to the former borrower. The rents naturally would be less than the previous mortgage payment. Read Wall Street Journal story on the program.

With the alternative of eviction, some troubled borrowers may find such a deal the best option in a bad situation.

Dustbiters 0

The FDIC has stirred to life again and begun to dine, leaving scraps of banks in its wake. Among the orts: