Masters of the Universe category archive

Mitt the Anointed 0

At the Guardian, Jason Farago argues that Mitt the Flip’s nomination is a done deal. He points to the one issue on which Mitt has not flipped: his unwavering loyalty to and identification with the corporate masters of the Republican Party and his belief in plutocracy uber alles.

(snip)

The fiction that Romney doesn’t believe in anything shows just how successfully the business absolutism he espouses has positioned itself outside ideological terms – beyond question, self-evident.

Follow the link for the rest.

Meanwhile, Field, who did part of his growing up in Michigan, remembers Mitt’s father:

To measure how far fell the apple from the tree, remember that George Romney made his pile by building a company. Mitt made his by destroying companies.

Developer Magic in Queens. Really? 0

Like Savoir Faire, the touching faith in developer magic is everywhere, even in Queens.

For those of you who have visited New York, how many of you have visited boroughs other than Manhattan?

I have, if you can call having a gig at Sunnyside Yards (which I reached by catching deadheads from Penn Station to the yards), attending a Yankees games (Yankee Stadium is maybe two blocks into the Bronx), or driving through Staten Island and Brooklyn on the way to Amityville (yes, I’ve been to Amityville) “visiting other boroughs.”

Via Atrios.

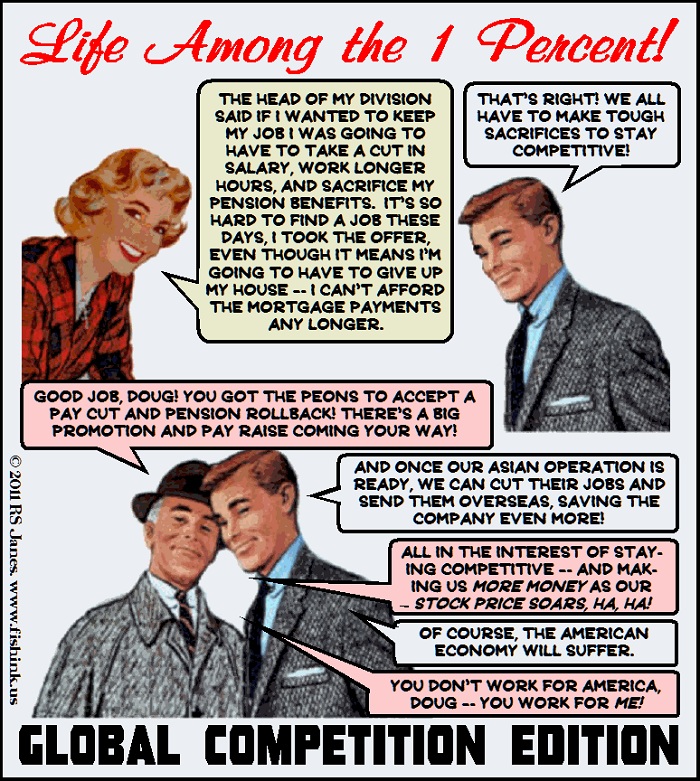

The One Percent Solution 0

Empathy schmempathy.

Fudging the Costs of Endless War 0

No account accountants.

The Entitlement Society 0

Thom Hartmann compares the bonus babies with the homeless babies.

Dustbiters 0

After a break of over a month, the FDIC is again remastering the universe.

All gone:

And, for desert . . .

Pastoral Newtonian Agricultural Paradises 0

Bloomberg investigates child labor in the Victoria’s Secret supply chain.

Try reading the whole thing. If you can get all the way through it at the first sitting, please let me know.

Spare the rod, spoil the child, eh, what?

No doubt, it warms the cockles of Newt the Gingrinch’s heart, already two sizes too small, to read of a work ethic’s being inculcated in children.

Aside:

The reporters mention Victoria’s Secret over and over in the story. By the time I was half-way through it, I was thinking, “Get a room already.”

Victoria’s Secret is certainly not alone in not seeing what is before its face. In corporate America, the concept of a “greater good” than bonuses and country club memberships is but a memory.

OWS out of Sight out of Mind 0

Margot Ford McMillen explains why Occupy Wall Street sites must be eliminated.

Their existence offends delicate sensibilities.

Buy some pepper spray stock, then click to read the rest.

High Finance for Dummies 0

Atrios explains how credit default swaps work.

Update from the Foreclosure-Based Economy 0

The benefits of foreclosures are oft understated. They can create and fund entire departments full of jobs. The Denver Post reports:

The public trustee system has generated huge profits by charging the public more than what’s needed to actually run its offices, according to financial documents provided by several counties and reviewed by The Denver Post.

What’s more, each trustee office has generated so much money that it has a bank account set aside with enough funds to maintain the office for a whole year — salaries included — in the unlikely event that not a single foreclosure gets filed.

More examples of lien largesse at the link.

Picking Pockets Any Way They Can, Have Cake Eat It Too Dept. 0

Depreciation is an economic and accounting concept that allows businesses to spread out the cost of a durable asset, such as a bulldozer, over time for tax and accounting purposes.

Delmarva Power wants to turn it into real money.

The meters provide Delmarva with remote access to meters, eliminating the need for readers to physically visit the meters to read them. It also allows the utility to check remotely if a home or business is receiving power, as it did during Hurricane Irene. That means earlier notice of outages.

The installation cost the utility $72 million, and Delmarva reports much of that was offset by savings, such as by no longer using meter readers. In Delmarva’s $31.8 million PSC rate case, the utility said it would only seek $174,000 immediately.

But in the filing, Delmarva also asked the PSC to create a process that would later allow them to recoup what is currently estimated as $39 million associated with the meters, over 15 years.

(snip)

Of Delmarva’s $39 million proposed charge to ratepayers, $26.5 million is to reimburse the company for the lost value of the old meters, which company officials said had not been fully depreciated.

So they upgrade the meters to save money, then want the customers to pay for the old meters because the old meters cost money when they were purchased Lord knows how many years ago and still have a value on paper.

Give them the kewpie doll for creative corporate conniving.

“Round and Round It Goes and When It Stops, You Get Hosed” 0

At Asia Times, Ellen Brown wonders why the Fed keeps shoveling money to banksters in the name of “increasing liquidity,” when banks are supposed to lend, not borrow.

She explains that it’s more Wall Street three-card monte. A snippet:

The answer is no. Today when banks make loans, they extend credit first, then fund the loans by borrowing from the cheapest available source. [4] If deposits are not available, they borrow from another bank, the money market, or the Federal Reserve.

Rather than loans being created from deposits, loans actually create deposits. They create deposits when checks are drawn on the borrower’s account and deposited in another bank. The originating bank can then borrow these funds (or others created by the same process at another bank) at the Fed funds rate – currently a very low 0.25%. In effect, a bank can create money in the form of “bank credit”, lend it to a customer at high interest, and borrow it back at very low interest, pocketing the difference as its profit.

If all this looks like sleight of hand, it is. The process has been compared to “check kiting,” . . . .

Read the whole thing.

Then invest your money in a slot machine in Lost Wages, Nevada; at least those games are regulated.

Corporate Raiders 0

Raiding employee pensions:

One of the most popular ploys is to use the bankruptcy court to undermine the bargaining position of labor unions. The latest firm to do so is American Airlines, which said it took the step to “achieve industry competitiveness.” This is corporate-speak for “we’re going to milk our employees dry.”

Full story at the link.

Update from the Foreclosure-Based Economy 0

The harsh truth is that the real estate bubble was a bubble.

It’s popped, not deflated. And it’s not coming back.

The number of local homeowners who were “underwater” on their loans rose 1 percent to 84,443 from June to September, according to CoreLogic, a Santa Ana, Calif.-based company that tracks mortgages nationwide.

For homeowners who aren’t in jeopardy of falling behind on payments, being underwater means they are tied to their homes – unable to sell without paying their lender the difference or negotiating a short sale.

Like the Tulip Bubble, all gone. The banksters are left with the money, having been made whole for their venality business “missteps” by the Fed; and the homeowners, left with wilted tulips.

Bombing far-away lands with strange-sounding names may be an effective distraction, but it ain’t fixing anything.

Support the Troops, Bankster Style 0

Selfishness has side-effects.

From the website:

Keith and Pat Garofalo, economic policy editor for ThinkProgress.org, discuss the latest report from the Treasury Department’s Office of the Comptroller of the Currency, revealing that 10 of the top U.S. lenders may have illegally foreclosed on up to 5,000 active duty service members.

Take the Money and Run 0

That would mean customer accounts are missing about 22 percent of their total of $5.4 billion. A shortfall of 11 percent had been previously estimated by a person with knowledge of probes into the firm’s collapse. James Giddens, the trustee, said yesterday that forensic accountants and investigators are working “around the clock,” and the estimate may change.

Know, grasshopper, that, behind that curtain, they have no idea what they are doing.

They know only that someone else will be left holding the bag.

Dustbiters 0

Two more banks disappeared from view yesterday.